Commercial insurance protects companies and their assets in case of lawsuits, natural disasters, theft, auto accidents and other shocks. Commercial insurance and business insurance are interchangeable terms for the same types of coverage.

Commercial insurance coverage will look different for every business depending on what it does, where it operates and many other factors. To protect your business, look for potential risks to figure out what policies you need.

02.

How does Commercial Insurance Work?

Commercial Insurance is meant to ease your financial burden when the unexpected happens. You’ll file a claim explaining what happened and what you’ve lost. Then, your insurer will issue a payment to help you recover your losses. If you’re being sued, your insurance company may handle your legal representation too.

Commercial insurance policies are made up of components that you may recognize from your personal insurance policies. These include:

Premium – the amount you pay monthly or annually to maintain your coverage.

Deductible – the amount you’ll have to pay before your insurance policy begins kicking in. In general, the higher your deductible, the lower your premium.

Policy Limits – the maximum amount your insurance policy will pay out during the policy period. You may have a per-occurrence limit, which is the total amount your insurer will pay out for one particular incident, as well as a total policy limit.

Exclusions – incidents your policy will not cover. Earthquake damage, for instance, is often excluded from commercial property insurance policies. And intentional damage or injury caused by your employees is usually excluded from general liability insurance policies.

Endorsements and Additional Coverages – add-ons to an insurance policy that extends its coverage. Endorsements and additional coverages will usually increase your premiums.

In most cases, you’ll need to already have a policy when an accident happens in order to be covered. Your policy period can usually begin the day you buy commercial insurance or the next day.

Commercial health insurance refers to health insurance that isn’t provided by the government. Business owners may offer their employees this type of coverage, typically via small-business group health insurance plans. These plans distribute risk among the whole group of employees, resulting in lower premiums than each employee would pay if they bought individual coverage. In general, small-business health insurance is provided by health insurance companies, not commercial insurance companies.

05.

More about General Liability Insurance

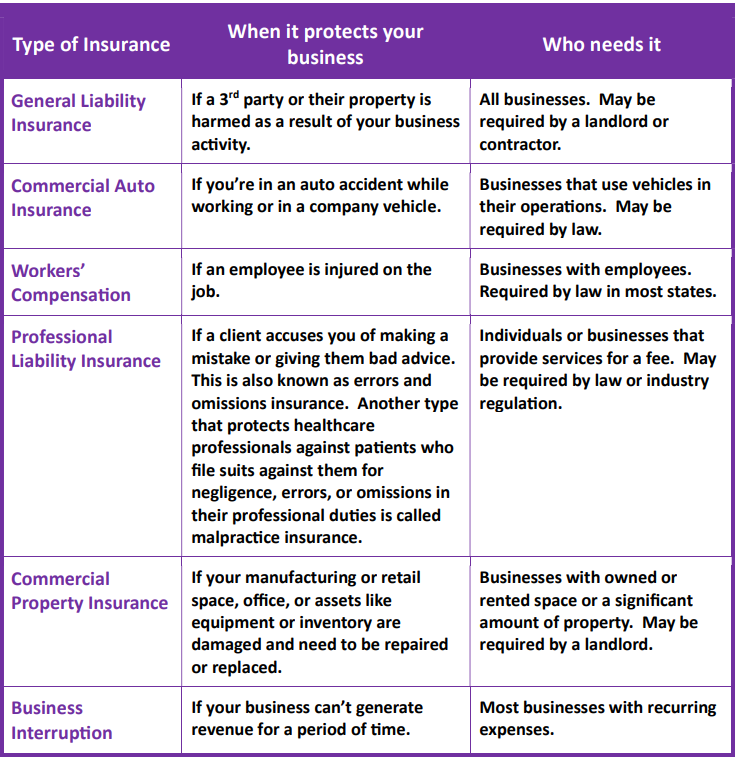

General Liability Insurance is one of the most common and basic types of insurance for businesses. It is an insurance coverage that protects business owners, and their businesses from 3rd party claims which involve property damage and bodily harm or injury. This coverage protects business owners and pays for the cost of litigation, bonds, settlements, and judgments as posted by the courts to the extent of the policy limit.

All businesses operate in an increasingly litigious society, and this also increases their need to understand what is general liability insurance coverage. Even if it may be difficult to imagine a situation where you are likely to face a claim from a 3rd party, insuring your business against such unforeseen factors and events is wise. While the type of business, risk factors and your coverage needs, it is still relatively inexpensive. This is very affordable compared to the amount of money you would spend “out-of-pocket” in legal fees and compensation in the event that your business is sued.

Worker’s compensation is a government-mandated program that provides benefits to workers who become injured or ill on the job or as a result of the job. It is effectively a disability insurance program for workers, providing cash benefits, healthcare benefits, or both to workers who suffer injury or illness as a direct result of their jobs.

In the United States, worker’s compensation is handled primarily by the individual states. The required benefits vary greatly state by state.

Worker’s compensation benefits may include partial wage replacement for the period during which the employee cannot work. The benefits may also include reimbursement for healthcare services and occupational therapy.

Most workers’ compensation programs are paid for by private insurers, from premiums paid by the individual employers. Each state has a Worker’s Compensation Board, a state agency that oversees the program and intervenes in disputes.

To determine the ideal types of commercial coverage for your needs and structure, contact us today to schedule a time to review your situation to find the right coverage.

Get a Free Quote

Insurance and Wealth Building

Please fill out your contact information. One of our agents will reach out to you soon. We look forward in helping you!